Financing a tow truck is crucial for automotive businesses such as local auto repair shops, car dealerships, and property managers. These industries often face financial challenges, especially when it comes to acquiring the necessary equipment to operate effectively and serve their customers. Understanding the right tow truck financing options can alleviate some of this stress and open doors to new opportunities. With various commercial financing options available, businesses can find tailored solutions that work within their budget constraints and operational needs.

Investing in a reliable tow truck can enhance service offerings, improve customer response times, and ultimately lead to increased revenue. However, the initial costs can be daunting, especially for small businesses that operate on tight margins. By exploring financing avenues, businesses can secure the necessary funds to acquire quality tow trucks, ensuring they remain competitive in a challenging market. Addressing these financial considerations with empathy and pragmatism helps business owners navigate the complexities of resource acquisition and lays the groundwork for future growth.

Financing Options for Tow Trucks

Financing a tow truck can seem overwhelming, but understanding the various options available can make the process easier and more manageable. Here are some of the most accessible financing methods for tow truck operators:

-

Tow Truck Loans: Traditional loans are a common choice for businesses looking to purchase a tow truck. These loans allow you to borrow a sum to purchase the vehicle, often with competitive interest rates and terms ranging from 3 to 7 years. Lenders typically require proof of business income and a minimum credit score around 600. More details can be found in this 2023 guide to tow truck financing.

-

Leasing Options for Tow Trucks: Leasing is an attractive alternative, especially for startups and businesses wanting to reduce upfront costs. With leasing, you make monthly payments without owning the vehicle outright. It allows for easier upgrades and better cash flow management. Notably, leasing can reduce initial costs by up to 40% compared to buying outright, making it favorable for those who prefer lower financial burdens.

-

Financing Through Dealerships: Many towing businesses opt for financing through dealerships, which often provides seamless transactions and convenience. Dealerships may offer in-house financing options, that include benefits like maintenance packages and lower interest rates. This method is appealing because it combines purchasing and financing in one step, preserving capital for operational needs.

Each financing option comes with its own pros and cons, and it’s essential to evaluate based on your business needs and financial situation. For additional insights on fleet safety and operation, consider checking out our emergency preparedness strategies.

Financing a tow truck offers numerous benefits, especially for local auto repair shops, car dealerships, property managers, resort operators, and commercial fleet operators. One of the key advantages is improved cash flow. By spreading payments over time, businesses can avoid the burden of a large upfront investment, allowing them to allocate resources more effectively while still acquiring essential towing equipment that boosts service capabilities. This financial flexibility enables auto repair shops to expand their services, enhancing customer satisfaction by providing quick towing and pick-up services, which can lead to increased revenues. Moreover, dealerships benefit from rapid vehicle delivery and repossessions, while property managers can respond swiftly to stranded vehicles on-site. Financing also allows businesses to acquire newer, more fuel-efficient models equipped with the latest safety features, translating into lower maintenance costs and improved operational efficiency. Learn more about essential fleet emergency response strategies and how financial flexibility can drive growth for your business.

Addressing Common Concerns About Tow Truck Financing

When it comes to financing a tow truck, many individuals and businesses encounter common concerns that can lead to misconceptions. Understanding these issues can save you from potential pitfalls and ensure that you get the best financing deal. Here, we’ll address some of the most frequent concerns, including interest rates, credit requirements, and hidden fees.

Interest Rates

Interest rates for tow truck financing can vary significantly based on your credit score and the lending institution’s terms. In 2023, interest rates typically ranged from 6.99% to 18.99%. For example:

| Credit Score Category | Interest Rate |

|---|---|

| Excellent Credit (800+) | 6.99% |

| Good Credit (700-799) | 8.5% |

| Fair Credit (650-699) | 11% |

| Bad Credit (600-649) | 15% |

| Poor Credit (below 600) | 18.99% |

Average Interest Rate: Approximately 9.2%

(Source: Real-time data from financial lending platforms and credit reporting agencies)

If you’re concerned about securing the best rate, it’s prudent to check your credit report beforehand. A higher credit score not only reduces your interest rate but can open doors to better financing options.

Credit Requirements

Many lenders require a minimum credit score of 650 for approval. However, it’s essential to note that some alternative lenders may accept scores as low as 600, albeit with higher interest rates. This flexibility can be a good option for small operators or those who are just starting but often comes with added costs or less favorable loan terms.

Hidden Fees

Another concern many borrowers share is the possibility of hidden fees associated with tow truck financing. Fees can include:

- Application Fees: Usually ranging from $100 to $300.

- Processing Fees: May vary by lender.

- Origination Fees: Up to $500 depending on the lender.

- Insurance Premiums: Often bundled into the financing deal but can drastically increase your total costs.

To avoid surprises, always ask for a detailed breakdown of all fees before signing any loan agreements. Reviewing the full loan agreement with a fine-tooth comb can help identify any potential red flags.

Conclusion

Understanding these financing terms can significantly enhance your likelihood of making an informed decision. Whether you are a local auto repair shop needing to expand your fleet or a commercial fleet operator, addressing these concerns can pave the way for smoother financing. If you’re looking to learn more about managing your financing needs, check out our emergency preparedness tips for island fleets or our strategies for essential fleet emergency responses.

| Lender | Interest Rate | Loan Term | Special Requirements |

|---|---|---|---|

| Bank of America | 6.5% – 14% | 3 – 7 years | Minimum 2 years in business, stable cash flow, business tax returns. |

| Kabbage | 6% – 35% | 3 – 7 years | Credit score > 680, at least 20%-30% down payment. |

| Lendio | 7% – 18% | 5 – 7 years | Personal/business credit report, business plan, vehicle evaluation. |

| Direct Manufacturer | Not specified | 5 – 10 years | Dependent on manufacturer, flexible repayment options available. |

| Online Lending Platforms | 7% – 20% | 5 – 7 years | Varies by lender, but usually requires proof of cash flow. |

Comparison Summary

This table provides a quick reference for evaluating financing options for tow trucks. Each lender varies in terms of interest rates, loan terms, and special requirements, making it crucial for businesses to assess their individual needs when selecting a lender. For more information on essential fleet emergency response strategies or emergency preparedness for island fleets, feel free to visit these links.

“Financing my tow truck was the best decision I could have made! With the added capital, I was able to expand my fleet and increase my services. Now I can serve more clients and get higher profits-it’s a game changer!”

- Jessica, Owner of Island Tow Services

Success stories like Jessica’s highlight the practical benefits of financing. When the right tools and equipment are accessible, local businesses thrive, paving the way for community growth and resilience. For further insights on enhancing your operational resilience, check out Emergency Preparedness for Island Fleets and Essential Fleet Emergency Response Strategies.

As we wrap up our exploration into how to finance a tow truck, it’s crucial to remember that the right financing can transform your business. For auto repair shops, car dealerships, property managers, resort operators, and commercial fleet operators, Summit Fairings stands ready to support your quest for premium tow truck financing. The opportunities presented throughout this article are not merely ideas; they are gateways to enhancing your operational efficiency and service offerings.

Imagine how transforming your fleet with new tow trucks can boost your market competitiveness, streamline your operations, and bolster your reputation within the community. When assessing your financing options, whether through SBA loans, manufacturer financing, or alternative funding, acting decisively can set you apart from competitors.

Don’t wait-seize the opportunity to elevate your business. Start today by reaching out to us for tailored financing solutions that meet your unique needs. Finance a tow truck that’s equipped to elevate your service capabilities and meet the demands of your customers. The time to take action is now-transform your machine today and secure your place as a leader in the towing industry!

Learn more about available financing options and take your first step toward fleet enhancement.

Understanding how to finance a tow truck can be essential for local auto repair shops, car dealerships, property managers, resort operators, and commercial fleet operators. Here are some common questions and clear answers regarding tow truck financing, tailored to your needs.

1. What is the best way to finance a tow truck?

The best financing option often depends on your business’s financial situation and credit profile. Here are a few popular choices:

- Bank Loans: Established operators with good credit can secure competitive rates, starting as low as 4.5%. It’s advisable to provide a solid business plan and financial records.

- Equipment Leasing: This option is ideal for those looking to preserve capital. Leasing typically has terms between 36 to 72 months with fixed payments, allowing businesses to upgrade equipment frequently.

- Specialized Lenders: Many lenders offer tailored financing solutions between 5% and 9%, depending on the credit score and other business factors. This can be a quicker method of obtaining funds for new and used tow trucks.

Learn more about financing options.

2. What are the typical interest rates for tow truck financing?

Interest rates for tow truck financing can vary greatly based on the borrower’s creditworthiness and market conditions:

- Qualified Applicants: For those with excellent credit (700+), interest rates can be as low as 4.5%.

- Fair Credit Borrowers: Individuals with fair credit (600-650) may face rates ranging from 7% to 10%.

- Average Range: Most borrowers can expect rates between 5% and 9%, particularly for loans secured with collateral.

Recent data suggests that most lenders also require tangible financial evidence, such as at least two years of business financial statements, and a minimum annual revenue of $100,000.

3. How much should I put down for a tow truck loan?

It’s generally recommended to make a down payment of at least 20% of the truck’s purchase price. This reduces the loan amount needed and can help negotiate better terms and rates. Higher down payments may also positively affect interest rates available to the borrower.

4. What documentation is needed for financing?

Most lenders will require:

- Proof of Revenue: Financial statements showing business viability.

- Business Plan: A detailed plan that includes how the tow truck will enhance your operations.

- Personal Credit Information: Lenders will often review both business and personal credit scores.

5. Can I get financing for used tow trucks?

Yes, financing for used tow trucks is widely available. However, rates may vary slightly compared to new trucks based on the truck’s condition, age, and mileage. It’s crucial to get a thorough inspection and provide documentation on the vehicle’s history.

For more insights on managing your fleet and ensuring safety, check our articles on emergency preparedness for island fleets and fleet emergency response strategies.

Conclusion

Financing a tow truck is a significant decision that requires careful consideration of available options, interest rates, and necessary documentation. By understanding these facets, local businesses can make more informed choices that fit their operational needs.

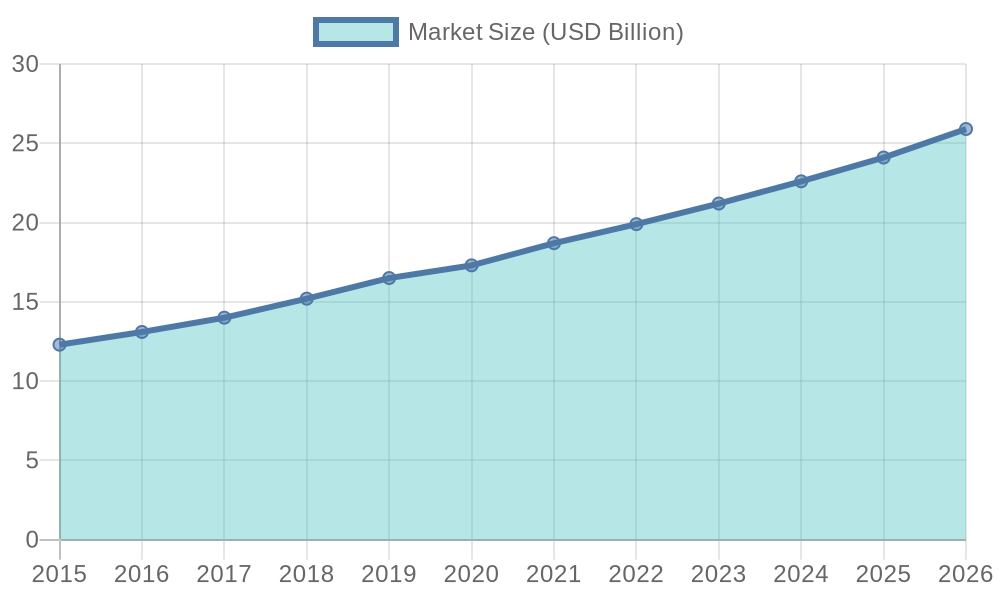

Tow Truck Financing Trends from 2015 to 2026

The chart illustrates the growing interest in tow truck financing over the years, highlighting:

- Increasing market size, projected to reach $25.9 billion by 2026.

- The trends towards leasing and flexible repayment plans as preferred financing options.

- An upward trend in financing tailored to meet the evolving needs of small and medium-sized businesses.

For more insights about financing strategies, you can learn more about emergency preparedness for island fleets or investigate essential fleet emergency response strategies.